Navigating the complexities of personal finance can be daunting for young professionals just starting their careers. With the right strategies, however, managing money effectively and setting the stage for future financial stability becomes achievable. This article explores essential personal finance tips tailored for young professionals, highlighting current trends and offering insights into future financial planning.

1. Embrace Financial Education

The first step towards effective financial management is understanding the basics of personal finance, including budgeting, investing, taxes, and debt management. Many young professionals may not have had formal education in managing finances, making it crucial to seek resources that can offer guidance. Websites, podcasts, and blogs dedicated to personal finance are invaluable tools that can provide the necessary knowledge to make informed financial decisions.

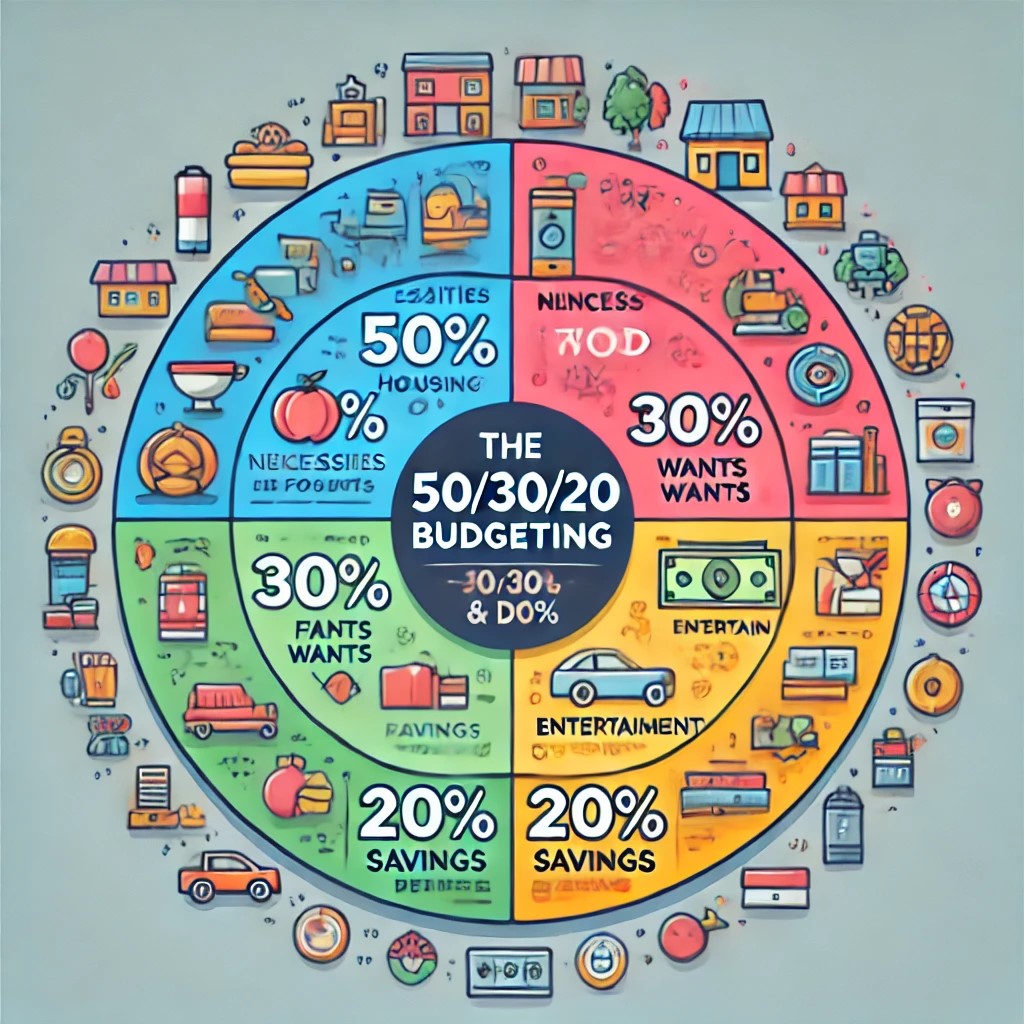

2. Start Budgeting Early

Creating and sticking to a budget is fundamental. It helps in tracking spending, saving, and investing habits. The 50/30/20 rule—allocating 50% of income to necessities, 30% to wants, and 20% to savings and debt repayment—is a popular strategy that can help young professionals manage their finances efficiently. Budgeting apps and tools have also become indispensable in providing real-time insights into financial habits and helping track financial goals.

3. Build an Emergency Fund

One of the most advised financial strategies is the establishment of an emergency fund. Ideally, this should cover three to six months of living expenses and be readily accessible. This fund acts as a financial buffer against unexpected events such as medical emergencies, job loss, or urgent home repairs, providing security without the need to incur high-interest debt.

4. Manage Debt Wisely

Many young professionals start their careers with significant debt, primarily from student loans. Understanding the terms of these debts, such as interest rates and repayment schedules, is crucial. Prioritizing high-interest debt and exploring refinancing options can reduce the interest burden significantly. Additionally, avoiding high-interest credit card debt by paying balances in full each month is a wise practice.

5. Invest in Your Future

Investing early is another critical component of financial planning for young professionals. Thanks to the power of compound interest, even small, regular investments can grow significantly over time. Employer-sponsored retirement plans, such as 401(k)s, often match contributions, which can boost retirement savings. Learning about different investment vehicles and considering long-term goals when choosing investments can maximize returns.

6. Plan for the Long Term

While it's important to manage current finances, planning for the future is equally crucial. This includes setting goals for buying a house, saving for retirement, or funding future education. Financial planning services and tools can offer personalized advice based on individual financial situations and goals.

Conclusion

For young professionals, mastering personal finance is a dynamic, ongoing process that requires education, consistent effort, and adaptability. By implementing sound financial habits early on, young professionals can set a foundation for long-term financial health, ensuring that they are well-prepared to meet their current and future financial challenges head-on.